| INTEGRATIVE INSIGHTS ON EMERGING OPPORTUNITIES |

Integrative research means our extensive company research informs every thesis and perspective. The result is deep industry knowledge, expertise, and trend insights that yield valuable results for our partners and clients.

TECHNOLOGY / SAAS WHITE PAPERS

|

Quarterly insights: Software as a Service

Growth expected to slow further; group underperforms market

The market and business disarray caused by the tariff war has made it difficult to assess prospects for many sectors, including SaaS companies. Our analysis of SaaS market conditions through March 31 may provide some helpful insight, since it provides a snapshot of conditions just prior to the tariffs. The average growth rate indicated by guidance for 2025 was 10.5%, down from 14.0% for 2024. Actual average revenue growth in 2024 was 15.1%, continuing a downtrend over the past few years. Our SaaS universe stocks declined 11.7% on average in the March quarter, underperforming the S&P 500’s 4.6% loss. Weakness was widespread with only 15 stocks in our 92-stock universe posting gains. The cybersecurity group led for the quarter, gaining 1.6% on average, and the Future of Work group lost only 2.6% on average in the quarter. The e-commerce group lost 17.6% on average, perhaps reflecting its relatively higher exposure to the risk of a soft economy. We also provide an overview of sector M&A activity and private placements during the quarter.

|

Quarterly insights: Cybersecurity

Sector maturation, narrower paths to success in still fast-growing market

We present our annual analysis of publicly traded, enterprise-focused cybersecurity firm performance. We highlight that 2024 aggregate revenue grew 16.7%, substantially slower than 2023’s 21.9% growth and 2022’s 30.8% growth. Average 2024 revenue growth was 16.6%, better than initial guidance for 15.1% growth on average; initial 2025 growth guidance is 13.4% on average. 2024 was a rare year of across-the-board profitability for our cybersecurity group and a rare year of across-the-board profit-guidance beats. We think this indicates the sector has matured to a point where profitability and revenue growth are more or less equally important to investors. We continue to see a trend toward increased market capitalization concentration among the publicly traded cybersecurity companies. However, innovative, cloud-native companies continue to outperform on growth, showing that technological differentiation and market focus remain powerful drivers of performance. We also provide an overview of sector M&A activity and private placements during the quarter.

|

Quarterly insights: Internet of Things

Five themes from CES 2025 and recent conversations

Based on our meetings and observations on the CES show floor and follow-up conversations with attending companies in the weeks since then, we identified five key themes for B2B IoT. First, our conversations suggest consolidation among connected car tech companies is already underway and set to accelerate. Second, while in-car payment is a logical use of vehicles’ embedded connectivity and digital capabilities and a natural part of the software-defined vehicle evolution, we think it makes most sense for activities that are clearly vehicle related. Third, we continue to see progress in energy harvesting technology and expect it to see strong adoption eventually. Fourth, we expect autonomy backup technology to become an industry standard for all autonomous programs. Lastly, we see a surprising number of IoT solution companies seeking to acquire connectivity assets in the already-consolidating MVNO market. We also provide an overview of sector M&A activity and private placements during the quarter.

|

|

Quarterly insights: Software as a Service

SaaS growth outlook higher, but valuations little changed

Our SaaS universe’s average enterprise value multiple of 2024 estimated revenue was 7.0 at the end of the December quarter, up from 6.8 last quarter. For 2025 estimated revenue, the average multiple was 6.0, flat from last quarter. Revenue growth in 2024 was expected to be 14.4% on average, up from 13.2% last quarter. In 2025, revenue was expected to grow 13.6% on average, up from 13.0% last quarter. Correlations between enterprise value multiples of revenue and revenue growth rates remained at or near longer-term normal levels, but the gap between valuations for small- and mid-capitalization companies and larger-capitalization companies increased slightly as six of the largest capitalization companies gained more on average than the overall universe. Our SaaS universe stocks appreciated 18.9% on average in the quarter, far ahead of the S&P 500’s 2.1% gain. Merger and acquisition activity among the public companies focused on smaller names. We also provide an overview of sector M&A activity and private placements during the quarter.

|

Quarterly insights: Enterprise productivity

Fraud fighters: Tech innovators address increasingly sophisticated, growing threats

At several conferences during the fourth quarter, we were astounded by the prominence of fraud as a major challenge for participants and by the proliferation of innovative technologies to combat this growing epidemic. Traditional fraud prevention efforts that depend on human attention can’t keep pace with the frequency and velocity of today’s financial crimes. Financial institutions and other businesses have concluded they need more advanced tools to combat fraud. Fraud-fighting businesses are increasingly stepping up to meet this demand in a market expected to grow by more than 20% annually and reach nearly $300 billion by 2032. We briefly profile some of the best ideas we saw among fraud-fighting technology providers at these conferences. We also provide an overview of enterprise productivity publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Cybersecurity

Challenges and promise of AI in cybersecurity

We reflect on both the frustrations and successes we’ve heard about AI in cybersecurity. The biggest hope for AI in cybersecurity is that it can prevent attacks, detecting and potentially blocking novel attacks before they can cause damage; however, such solutions have not been the silver bullet they were hoped to be. In the near-term, we believe it will be challenging to implement AI to detect zero-day and novel threats due to the unpredictable nature of these attacks and the difficulty AI has in distinguishing harmless anomalies from true threats. Efforts to address these shortcomings with information transparency also face challenges. We’re seeing the most success among solutions that use AI to improve cybersecurity teams’ ability to interact with traditional cybersecurity approaches. By bridging the gap between technical complexity and human understanding, these AI solutions streamline security operations centers, enabling teams to be more efficient and effective. We also provide an overview of cybersecurity publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

.jpg)

|

Quarterly insights: E-commerce optimization

Shoptalk Fall: Four themes from the 2024 show

Despite being smaller than the other two Shoptalks, Shoptalk Fall featured many high-quality e-commerce technology companies and knowledgeable industry participants. We identified four key themes for e-commerce tech and highlight some of the companies benefitting from them. First, we saw a growing recognition that the true value of AI in e-commerce lies not in AI itself, but in how it enhances offerings and plays within larger solution frameworks. Second, unified communication in e-commerce has become table stakes, and we think the new frontier in e-commerce communication lies in technologies that enable rich consumer experiences entirely within message formats like text and email. Third, the evolution toward fully converged in-store and e-commerce continues, driven mainly by brands’ and retailers’ acute and unmet need to precisely attribute consumer sales and engagement to sales and marketing spend. Lastly, while technology to address e-commerce product returns remains focused on optimizing returns processing and logistics, we think the larger, long-term opportunity lies in technologies that substantially reduce returns by addressing their root causes. We also provide an overview of e-commerce optimization publicly traded stock performance and valuation, sector M&A activity, and private placements over the past two quarters.

|

White paper: Internet of Things

MVNO proliferation puts spotlight on competitive differentiation, ancillary capabilities

The number of mobile virtual network operators (MVNOs) serving the IoT market appears to have increased dramatically over the past few years. We attribute the perceived increase primarily to four factors: The compelling opportunity for MVNOs in the IoT market, loss of interest in the IoT market among the large mobile network operators, the appearance of mobile virtual network enablers (MVNEs), and reduced barriers to entry. We think the most successful MVNOs will be those that move beyond simply reselling connectivity to provide unique added value to their IoT customers. We detail several such strategies being pursued by MVNOs and companies in adjacent segments. These strategies often blur the boundaries of traditional value chains. We highlight companies pioneering these promising strategies. We also highlight key trends and factors to watch.

|

|

Quarterly insights: Software as a Service

Valuations rise again with modest SaaS stock appreciation

Our SaaS universe stocks gained 3.0% on average in the September quarter, underperforming the S&P 500, which continued to make new highs with a 5.1% gain. While the average gain was low, results varied widely for many stocks in our SaaS universe, with eight stocks gaining over 30% and six losing over 30%. Once again, positive performance generally depended on good earnings and solid forward guidance. The average SaaS enterprise value multiple of estimated 2024 revenue at the end of the quarter was 6.8, up from 6.4 last quarter. For 2025, the average multiple was 6.0, up from 5.6 last quarter. Revenue growth in 2024 was expected by analysts to be 13.2% on average, down from 13.4% last quarter. In 2025, growth was expected to decrease to 13.0% from 14.2% last quarter, reflecting the influence of softer guidance. We also provide an overview of sector M&A activity and private placements during the quarter.

|

Quarterly insights: Software as a Service

Valuations reverse lower, 2025 growth expectations also down

Our SaaS universe’s average enterprise value multiple of 2024 estimated revenue was 6.4 at the end of the June quarter, down from 7.1 last quarter. For 2025 estimated revenue, the average multiple was 5.6, down from 6.1 last quarter. Revenue growth in 2024 is now expected to be 13.4% on average, up from 13.0% last quarter. In 2025, revenue is expected to grow by 14.2% on average, down from 15.0% last quarter. Correlations between enterprise value multiples of revenue and revenue growth rates have returned to more normal levels above 0.6 in the past two quarters. The six largest-capitalization SaaS companies outperformed our general universe. While the outperformance of these larger SaaS names may continue for a while based their relatively high current growth rates, longer-term we expect the growth advantage to return to smaller capitalization stocks that can maintain higher growth rates. We also provide an overview of sector M&A activity and private placements during the quarter.

|

Quarterly insights: Enterprise productivity

Will this tenant pay? Tech helps find a better answer

Consumer financial stress resulting from the long-term shortage of housing in the United States and consequent housing inflation appears to be driving an increase in multifamily housing tenant fraud, which was already widespread. Traditionally, many property managers have used credit scores to evaluate prospective tenants, but credit scores' backward-looking nature means they don't capture current financial stress, and credit scores don't verify income. These challenges have accelerated the growth of an industry of alternative credit qualification platforms. These platforms leverage the internet's ubiquitous connectivity with software that taps consumer data sources that previously were impossible to access inexpensively and at scale, such as employment income, rent payment history, and personal expenditures. We profile 12 companies using alternative data to help landlords and property managers get a better answer to the critical question: Will this tenant pay? We also provide an overview of enterprise productivity publicly traded stock performance and valuation, sector M&A activity, and private placements during the past two quarters.

|

Quarterly insights: E-commerce optimization

Rise of harmful internet bots underscores need for effective technology solutions

The pandemic’s acceleration of e-commerce growth has made it more attractive than ever for a shadow industry of ethically compromised entrepreneurs to siphon sales from legitimate e-commerce sites using automated software called scalper bots. Harmful bots altogether, including outrightly criminal bots, represented 32% of all internet traffic as recently as 2023, up from 24% a decade ago. The damage wrought by scalper and other bots that divert sales from legitimate sites ranges from higher costs and frustration for consumers to lost sales and reputational damage for legitimate sellers. While many have advocated for legislation and regulation to stop bots, little has come from these efforts. We think companies offering technology solutions to counter bots offer a much more effective and immediate path to minimize the bot threat. We profile several innovative companies addressing the bot threat in four categories: CAPTCHA, multi-factor authentication, and behavioral analysis technology solutions that help sellers defend against bots and offensive bots that empower consumers. We also provide an overview of e-commerce optimization publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Software as a Service

SaaS companies expect growth to slow further in 2024

The average growth rate indicated by guidance for 2024 was 13.8%, down from 15.9% for 2023. Actual revenue growth in 2023 was 16.9%, well below 2022’s 28.9% growth, and the 1.0 point difference between the 2023 guided and actual growth rates was unusually low. Our SaaS universe stocks declined 0.9% on average in the March quarter, underperforming the 10.2% gain for the S&P 500. Stock price performance dispersion was relatively high in the quarter, ranging from the Internet of Things (IoT) group’s 15.4% average gain to the Future of Work group’s 12% average decline. The average enterprise value multiple of estimated 2024 revenue was 7.1 at the end of March, up slightly from 6.7 at the end of December. Correlations between enterprise value multiples of estimated forward revenue and estimated forward revenue growth rates reverted to more normal levels. We believe the higher correlations reflect the fact that more small- and mid-capitalization SaaS companies participated in the market’s strength during the quarter such that enterprise value multiples of revenue better aligned with revenue growth prospects. We also provide an overview of sector M&A activity and private placements during the quarter.

|

Quarterly insights: Cybersecurity

Growth continues to slow with more focus on profitability

We present our annual analysis of publicly traded, enterprise-focused cybersecurity firm performance. We highlight that 2023 aggregate revenue grew 18.4%, substantially slower than 2022's 26.5% growth and 2021's 24.3% growth. Average revenue growth was 16.4%, somewhat below 2023 initial guidance for 18.5% growth on average; initial 2024 growth guidance is only 13.5% on average. We believe the revenue growth slowdown reflects cybersecurity companies heeding investors' desire for more focus on profitability. Should it continue for multiple years, we think investors may view a shift to slower sector growth, even if accompanied by greater profitability, as limiting the sector's long-term potential. However, we don't see anything in the threat environment to make us believe market growth will slow for an extended period, and we are hopeful that our public cybersecurity group will sustain double-digit revenue growth. We remain optimistic the market will continue to be open to many winners, including smaller companies. We also provide an overview of cybersecurity publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Internet of Things

CES now a key B2B IoT forum: Six themes from the 2024 show

CES 2024 featured an abundance of telematics hardware providers, video telematics solution providers, hardware-agnostic end-to-end IoT solutions and many more types of B2B IoT companies. We expect CES to continue to rise in prominence as the most productive trade forum for B2B IoT companies. Based on our meetings and our observations on the show floor, we identified key themes for B2B IoT in six areas: artificial intelligence, energy harvesting technology, cameras, hardware strategies, sensor fusion, and robotics. We discuss each of these areas and highlight relevant companies. We also include an overview of IoT publicly traded stock performance and valuation, sector M&A activity, and private placements during the past quarter.

|

White paper: Go-to-market Tech 2.0

The First Analysis B2B GTM Framework: A deep dive into the granular categories and innovative companies

In this white paper, we delve deeper into the GTM industry, building upon our previous analysis of GTM growth drivers, market structure, GTM trends & themes. We provide an extensive overview of the seven phases comprising the GTM tech stack. Additionally, we explore the technologies that support each of these phases and profile more than one hundred innovative companies operating within this ecosystem.

|

Quarterly insights: Software as a Service

Expanding SaaS multiples became less correlated to growth outlook in Q4

Our SaaS universe gained 16.0% on average in the December quarter. The cybersecurity and data visibility groups continued to be the leading gainers. The SaaS average enterprise value multiple of 2023 estimated revenue increased to 7.8 from 6.6 last quarter. For 2024, the average multiple was 6.7, up from 5.6 last quarter despite an expected slowdown in growth to 13.3% from 15.8% last quarter. Correlations between revenue multiples and revenue growth expectations, which were already low by our historical measures, declined from the September quarter, suggesting the valuation gains in the quarter were based on factors other than fundamental growth prospects; we believe momentum was a big factor. We also provide an overview of SaaS publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Cybersecurity

Detection solutions prevent the spread of harmful deepfakes

Deepfake creation technology has evolved significantly from the rudimentary face swaps that first allowed everyday users to create low-quality deepfakes in the mid-2010s. Since then, deepfake creators, including bad actors, have developed a variety of creation methods, and the technology continues to evolve rapidly. Governments, individuals and corporations are eager to find ways to stop malicious deepfakes, given their sometimes enormous monetary and societal costs. Deepfake detection companies address this need. They essentially reverse engineer the deepfake creation process to identify manipulated content. The criteria for choosing among deepfake detection solutions vary based on use case. We discuss use cases in news media, law enforcement and other governmental functions, banking, and general commerce. Each differs in the level and type of deepfake detection it needs. We highlight a sample of large technology companies that offer some deepfake detection solutions and highlight some deepfake specialists, including three for which we provide detailed profiles. We also provide an overview of cybersecurity publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Future of work

HR integration tech helps companies win the best-of-breed vs. suite battle

Due to cyclical pressure on budgets, corporations in 2023 have tended to buy human resources (HR) software suites rather than best-of-breed solutions. In coming years, however, we believe long-term secular trends, such as increased demand for HR data insights and lower costs to develop purpose-built software for specific HR functions, will drive a reversion toward buying more best-of-breed applications. Seamless integrations are key to adopting best-of-breed solutions, as they enable data transfer and visibility among systems, cost-effective implementation, and harmonized workflows. Given the compelling return on investment from HR tech solutions and employers’ growing interest in tailored HR tools to address the long-term challenges they face in building and maintaining their workforces, we expect to see strong demand for software that enables cost-effective, continuous integration of HR tech solutions. We review some of the near-term and long-term trends driving this demand, discuss how integration technology will help companies shift to best-of-breed HR tech solutions, and profile several innovative HR integration tech platforms. We also provide an overview of future of work publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: E-commerce optimization

Customer review technology: Continued innovation means more opportunity

Today, basic consumer-facing review technology is considered a commoditized, mature area. However, there are areas of innovation where providers offer differentiated solutions. These areas represent compelling growth opportunities for emerging providers and their investors. Several factors are driving this innovation, including advances in machine learning and natural language processing technology, increasing e-commerce regulation, and growth in e-commerce's share of total retail sales. We map the market and explore five review technology subsegments in detail: core review data management platforms, vertical review platforms, social listening platforms, review data analytics platforms, and customer intelligence platforms. We highlight some key players in and adjacent to each area. We also provide an overview of e-commerce optimization publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Cybersecurity

Proliferating APIs expand attack surface for adversaries

Application programming interfaces (APIs) are a critical building block of modern software whose use has surged in recent years, making the importance of APIs for web traffic today hard to overstate. As a result, APIs have become key targets for attackers. Traditionally, entities have primarily used web application firewalls (WAFs) and API gateways to secure APIs from attackers. But while WAFs and gateways play crucial roles in security architectures, they have limits. The limits of WAFs and API gateways have highlighted the need for new approaches to safeguard against advanced emerging threats and have led to a new generation of API security platforms. We briefly profile 10 companies offering newer API security approaches, usually as part of a broader security or enterprise software platform. We provide more detailed profiles of six pure-play companies providing API security. We also provide an overview of cybersecurity publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Software as a Service

SaaS valuations contract as growth outlook weakens

The average stock in our SaaS universe declined 5.1% in the September quarter, modestly underperforming the S&P 500's 3.7% decline. The average enterprise value multiple of estimated 2023 revenue for our SaaS universe decreased to 6.6 from 7.0 last quarter. For 2024 estimated revenue, the average multiple was 5.6, down from 5.9 last quarter. The average expected 2023 revenue growth rate was 16.1% as of Sept. 29, down from 16.2% on June 30, and the average expected 2024 revenue growth rate was 15.8%, down from 17.1%. The data visibility group had an average gain of 4.7% and included both announced acquisitions in our universe. However, the cybersecurity group led with a 9.0% average gain. With correlations between revenue multiples and growth rates remaining low, there are many wide outliers. We also provide an overview of SaaS publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Enterprise productivity

From asset purchases to operations, tech still center stage in real estate

We identified two key themes at this year’s CREtech conference: First, increased interest rates have made it more imperative than ever for landlords to minimize their operating expenses. Second, the rate increases have reduced or eliminated room for error in the process of accurately assessing the profit potential of new real estate acquisitions. Technology remains at the center of the stage in efforts to address these challenges. Well-capitalized landlords are racing to implement technology-based strategies to lower their operating expenses. We’re also seeing a higher profile for technology companies that use artificial intelligence to locate and evaluate real estate investment opportunities. We highlight some technology-based solutions that manage utility costs using connected devices and related tools. We also highlight companies that offer software to automate and enhance the process of evaluating and prioritizing new property acquisition opportunities. We provide an overview of enterprise productivity publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

White paper: Go-to-market Tech

Evolution of strategies for optimizing enterprise growth

With the world’s rapid digital transformation since the 1990s, human social behaviors have forever changed, and as a result, business-to-business (B2B) buyer purchase patterns have shifted toward more digital-friendly, buyer- and peer-led multi-stakeholder processes. This shift has forced many sellers to meet buyers on buyers’ terms and establish new go-to-market (GTM) strategies. Gartner defines go-to-market strategies as plans that detail how organizations can engage with customers to convince them to buy their products and services and to gain a competitive advantage. This white paper analyzes GTM industry growth drivers, market structure, GTM trends & themes and presents the First Analysis GTM framework.

|

Quarterly insights: Internet of Things

Use of bodycams outside law enforcement set for dramatic rise

Law enforcement has been the most aggressive adopter of body-worn cameras. Over 70% of agencies across the United States have implemented a bodycam solution, realizing compelling benefits including increased safety for officers and the public they serve and increased transparency in policing. However, there are many sectors outside first responders that would benefit from deploying bodycams, and interest in deploying bodycams in such sectors has been building over the last few years. We believe this opportunity is at least 13 times the size of the first-responder market: There are more than 22.5 million potential bodycam users in other sectors. We detail the factors we believe are fostering growing demand for bodycams and identify strategies and capabilities that are likely to characterize the most successful companies addressing the growing opportunity. We also include an overview of IoT publicly traded stock performance and valuation, sector M&A activity, and private placements during the past two quarters.

|

Quarterly insights: Software as a Service

SaaS valuation multiples continued to recover in the June quarter

Our SaaS universe gained 9.6% on average in the June quarter and 30.9% in the first half of 2023. Substantially all the gain has been from expansion of enterprise value multiples of estimated revenue, to 7.0 on average for 2023 estimated revenue at the end of the June quarter from 5.2 at the end of 2022. The valuation framework we initially presented in 2019 suggests the 7.0 multiple is fair value now. The data visibility group had the largest average stock-price gain for the second quarter in a row, up 19.4% on average, as artificial intelligence continued to drive interest in the group. With correlations between revenue multiples and growth rates remaining relatively low, there are many interesting outliers. Given the recovery in valuation multiples, we were somewhat surprised that none of our SaaS companies were the subject of newly announced acquisitions in the quarter. We also provide an overview of SaaS publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Cybersecurity

RSA 2023 and Q2 highlights: Key insights and takeaways

We present our key takeaways from the 2023 RSA cybersecurity conference and our follow-up meetings and conversations during the quarter. AI, which has been used in cybersecurity for years, was a hot topic, but we were surprised to hear many attendees focusing on the challenges of using AI in cybersecurity. Generative AI in cybersecurity remains at an early stage, but attendees identified some areas where it is likely to be most useful in the near term. Expanding enterprise attack surfaces, increasing complexity, and expanding purviews for CISOs are all escalating cybersecurity challenges despite growing cybersecurity budgets. The worsening cybersecurity talent shortage is pushing enterprises to continue consolidating their cybersecurity solutions with fewer vendors and increase their use of managed cybersecurity services. We also provide an overview of cybersecurity publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Enterprise productivity

Multifamily landlords use leasing automation to counter economic hit of higher rates

The phenomenon of low interest rates lasted far longer than most expected but was destined to end eventually. As such, it was an inherently unstable foundation for long-term value in multifamily property portfolios and one over which landlords had virtually no sway. To offset the erosion of cash flow by higher interest costs, multifamily property landlords are racing to deploy technology that optimizes revenue and minimizes costs, helping ensure their cash flows remain stable or increase. One of the technologies that can yield substantial operating cost savings, productivity gains and revenue gains is leasing management software. Leasing management systems help landlords maximize the leads they ingest and help sales teams be as efficient as possible. We profile several companies that provide leasing management systems. Given prospects for sustained high interest rates, we expect these companies and other providers to see increasing demand for their solutions. We also provide an overview of enterprise productivity publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: E-commerce optimization

Generative AI to disrupt and see widespread adoption in e-commerce

While AI has long been used as an enabler in specialized software to automate and improve specific business processes, the debut of mass-market generative AI based on large language models has opened a new dimension for AI: It is the first highly visible application of advanced AI models that is accessible and easy to use, enabling workers at all levels across many industries to quickly receive coherent, well-written responses to brief questions or text prompts. We expect generative AI to permeate and disrupt virtually every industry, but given generative AI's distinctive ability to produce informative content directly usable by humans, we expect its impact to be perhaps greatest in e-commerce. Indeed, there are likely few applications of generative AI that don't relate in some way to e-commerce. We briefly review the context in which generative AI has evolved and then explore its applications across e-commerce content and communication types. We also discuss the key factors we expect will drive rapid and widespread adoption in e-commerce and the challenges companies will need to overcome along the way. Lastly, we discuss some of the future directions for generative AI in e-commerce. In nearly all these discussions, we highlight relevant innovative companies using generative AI to provide extra value to their clients in e-commerce applications and beyond.

|

Quarterly insights: Software as a Service

SaaS companies guide low for 2023; how much is conservatism?

Our SaaS companies that provided guidance for both 2022 and 2023 expect 2023 revenue to grow on average only about two-thirds as fast as they expected revenue to grow in 2022. The magnitude of guidance declines was relatively consistent across companies and groups, leading us to think conservatism is a significant factor. The average SaaS stock in our universe appreciated 19.4% in the March quarter, well ahead of the S&P 500's 7.0% gain. In our analysis of revenue multiples versus estimated revenue growth rates for 2023 and 2024, the correlations remained low at 0.49 for 2023 (down from 0.52 last quarter) and 0.38 for 2024. We provide an overview of SaaS publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Cybersecurity

Public players grew faster again in 2022, but guiding for a slowdown

We present our annual analysis of publicly traded, enterprise-focused cybersecurity firm performance. We highlight that 2022 revenue grew 26.4%, a slight acceleration from 2021's 24.4% growth and well above 2020's 18.0% growth, and that actual 2022 revenue exceeded initial guidance by an average and median 2%, suggesting overall demand was solid. Companies focused on cloud-based solutions were again the fastest growers, and fast-growing cybersecurity behemoths Fortinet (FTNT) and Palo Alto Networks (PANW) continue to evade the fate of slowing growth typically seen at the sector's largest players. Stock prices for the group declined by a much wider margin over the past year than the major indexes despite the strong revenue growth and despite the group beating 2022 revenue guidance on average. We attribute this to 1) a shift in investor sentiment toward favoring cash flow generation and profitability over growth and 2) 2023 revenue growth guidance that indicates a meaningful deceleration is anticipated. The two largest-market-cap companies (Fortinet and Palo Alto) now account for nearly half the group's total market capitalization, up from about a third a year ago. We also provide an overview of cybersecurity publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

White paper: Enterprise productivity

Technology for alternative consumer credit scoring will be a large and fast-growing market

Traditional consumer metrics, most notably FICO scores, are becoming inadequate as a basis for deciding whether to extend consumer credit. Lenders and other stakeholders increasingly understand this and are seeking ways to assess consumer creditworthiness more accurately. A wide range of alternative consumer metrics, including data from bank account statements, rent payment records and utility bill payment records, provide information that addresses this need, but for much of the history of consumer credit, it was impractical to use this type of data due to the cost and logistical challenges of collecting and analyzing it. In today's increasingly connected and digitized financial ecosystem, these barriers are shrinking, and innovative companies are using technology to offer consumer lenders credit analysis and decision tools based on these alternative metrics. Given the large size of the market for traditional consumer credit metrics (we estimate at least $5.6 billion annually) and the compelling value these tools can provide for consumer lenders, we think companies that provide these tools can grow quickly and achieve substantial scale as they displace the use of traditional consumer credit metrics and enable lenders to tap new consumer segments where they previously lacked sufficient information to make credit decisions. We think there is ample room for multiple winners and profile several companies leading this emerging segment.

|

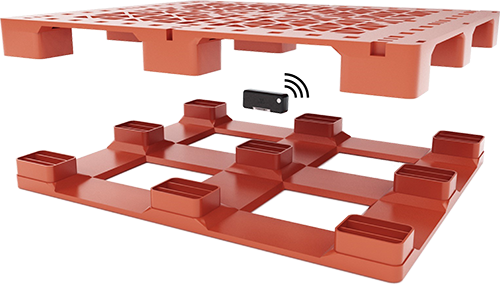

Quarterly insights: Internet of Things

Shift to condition monitoring to finally drive connected pallet adoption

The first generation of IoT solutions for wirelessly connecting pallets focused mainly on the value of the pallets themselves, only tracking location. This approach failed to gain traction because it offered insufficient return on investment, addressed too small a portion of the market, and suffered from high up-front costs and ongoing technology maintenance costs. A second generation of IoT pallet technology is emerging that overcomes these shortcomings. These solutions monitor the conditions pallets - and more importantly, their cargoes - experience on their journeys through supply chains. By monitoring conditions, such as temperature, vibration, shock and humidity, these solutions provide information that helps manufacturers, distributors, and shippers preserve the products pallets carry, which are typically much more valuable than the pallets themselves. We expect these solutions' broad and substantial appeal to help drive strong growth for companies providing second-generation pallet IoT solutions, and we profile several such companies. We include an overview of IoT publicly traded stock performance and valuation, sector M&A activity, and private placements during the past two quarters.

|

Quarterly insights: Software as a Service

Valuation multiples contract again, but correlation to forward growth highest in a year

The average stock in our SaaS universe declined 3.6% in the December quarter, underperforming the 7.1% gain for the S&P 500. Five companies gained over 30% and nine lost over 30% in our current 96-company universe, about the same as the tally in the September quarter. The average SaaS enterprise value multiple of estimated revenue was 6.3 for 2022, down from 6.9 last quarter, and 5.2 for 2023, down from 5.5 last quarter. The decline likely in part reflects a reduction in average 2023 growth estimates, from 22.5% last quarter to 19.2% as of Dec. 31, but also a continued correction from what we view as excessive valuation levels a year ago plus perhaps some tax-loss selling. The correlation between enterprise value multiple of 2023 estimated revenue and 2023 estimated revenue growth was 0.52, up from 0.48 last quarter. This was the highest correlation level for forward-year revenue figures we’ve shown since the December 2021 quarter. We provide an overview of SaaS publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Cybersecurity

Authentication tech: Secure or user friendly? Increasingly both

The weakness of password-only authentication for access to protected data is well known. Multifactor authentication (MFA) is a long-established way to address this weakness, but it wasn’t practical to deploy widely until the advent of cell phones and SMS for delivering second authentication factors. With nearly everyone owning a mobile phone today, MFA has become a familiar, regular, and highly trusted experience for most internet users. As MFA has become more prevalent, bad actors have directed their attention to defeating it and have developed relatively simple ways to compromise basic MFA. Organizations can respond by implementing enhancements that cost more and require more user effort, but there’s no one-size-fits-all solution. The key is finding the right balance between the value of the data being protected and the cost and user effort associated with different security levels. We discuss the evolution of MFA, its vulnerabilities, and some of the ways basic MFA can be enhanced to address those vulnerabilities. We provide a brief survey of prominent MFA solution providers. We also provide an overview of cybersecurity publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Future of Work

Large opportunity for employee coaching platforms helping win the war for talent

While the war for talent may cool in some sectors in the near term, long-term trends including aging populations, the increasing need for technology skills, and shifting personal values among younger workers suggest a truce is nowhere in sight. We expect recruiting, retaining and cultivating talent to remain a challenge that requires a growing arsenal of innovative technologies for building, developing and managing workforces. Regardless of economic conditions, we expect employers to increasingly adopt software-enabled employee coaching as a key part of that arsenal. Given coaching's compelling return on investment and employers' strong appetite for tools to address the long-term challenges to building and maintaining workforces, we expect to see continued strong demand for software-enabled coaching. We review some of the near-term and long-term trends driving demand, discuss how coaching platforms help in the war for talent, and profile several innovative employee coaching platforms. We also provide an overview of future of work publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: E-commerce optimization

Brands move toward VR and AR to deliver immersive e-commerce experiences

The metaverse is poorly understood and has failed to gain traction as a concept. We think key technologies underpinning the metaverse – virtual reality, augmented reality, and extended reality – have significant potential when applied to e-commerce to enhance the everyday experience of the billions of people who shop online. We expect brands and retailers to increasingly demand technologies that help them compete and increase sales by delivering more engaging, immersive online experiences. We discuss how these technologies work, key application areas, why sellers and consumers find them compelling, and which immersive technology provider strategies seem most likely to succeed. We profile several interesting immersive technology providers. We also provide an overview of e-commerce optimization publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Software as a Service

SaaS outperforms in volatile quarter; many big winners and losers

Our SaaS universe's average 1.6% stock price decline in the September quarter belies the market turmoil in our current 98-stock universe, as seven stocks gained over 30% and 10 stocks lost over 30%. The universe's average enterprise value multiple of 2022 estimated revenue declined to 6.9 from 7.5 last quarter. The reduction reflects a combination of stock price declines and generally increasing 2022 revenue estimates, as the average 2022 estimated revenue growth rate increased to 30.0% from 28.8% last quarter. While the correlations between the universe's estimated revenue growth and revenue multiples improved from the very low levels last quarter, we still view the correlations as abnormally low. An eventual reversion to more normal levels will likely be one of the key drivers of future SaaS stock price moves. We provide an overview of SaaS publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Cybersecurity

Evolution of network-based security favoring network detection and response

Cybersecurity threats have evolved to evade many of the basic building blocks of network-based security systems. We believe newer network detection and response (NDR) solutions will increasingly address these new threats and grow to become another major building block of network-based security systems. Increased computing power that enables cost-effective network monitoring at scale, as well as advances in machine learning and artificial intelligence, have made NDR a powerful and accessible cybersecurity tool. In this report, we provide a high-level overview of how NDR systems work and why they are needed. We discuss key areas where NDR systems differentiate themselves, such as in decryption capabilities, and profile four key NDR solution providers. We also provide an overview of cybersecurity publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Enterprise productivity

Higher interest rates mean higher interest in tech for mortgages

One might expect the recent rise in interest rates would be a negative event for companies selling technology to the mortgage industry, which has shed workers as refinancing demand has declined. We believe the opposite is true for several reasons. Most importantly, as interest rates shift rapidly in the current, more volatile environment, it is more challenging than ever for now-downsized mortgage sector companies to respond quickly and efficiently to all their potential customers. Lenders have concluded technological innovation can make their mortgage volume capacity more independent of staffing levels. They also see opportunities to use technology to reduce overall loan origination costs and thereby provide flexibility to price more competitively. These factors and others point to increased demand for technology that can automate and improve mortgage industry processes. We profile several innovative companies rising to the challenge. We also provide an overview of enterprise productivity publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Software as a Service

SaaS valuations continue to decline despite solid growth outlook

Our SaaS universe stocks dropped 30.3% on average in the June quarter, and the average SaaS company enterprise value multiple of estimated 2022 revenue at the end of the quarter dropped to 7.5 from 11.2 at the end of the March quarter and to 5.9 for 2023 estimated revenue from 8.7 last quarter. At the same time, the estimated revenue growth outlook for our universe is essentially unchanged. The correlations between growth rates and revenue multiples continued to deteriorate during the quarter. We believe this reflects SaaS stocks being indiscriminately dumped by investors. Higher correlations prevailed for years prior to 2022. To the extent the correlations revert toward the norm, we think it will be mainly due to investors becoming more discriminating in valuations rather than a re-rating of the entire sector. As such, we believe individual stock selection could be more highly rewarded than buying a SaaS index. We provide an overview of SaaS publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Future of Work

Mentoring and coaching tech: Key to scaling learning and development

While we expect the labor market to cool from its recent torrid levels, the fundamentals underpinning the long-term war for talent aren't going away anytime soon. That means employers continue to become more attuned to the importance of personalized learning for organizational performance and employee engagement and retention. A key mode of personalized learning is coaching and mentoring. We believe employers are increasingly investing in coaching and technologies that enable well-targeted mentoring for employees below the C-suite level. This portends a favorable environment for companies that enable employers to deliver coaching and mentoring in a more effective and targeted manner. We examine the underpinnings of this trend and profile several companies that automate elements of coaching and help optimize internal mentoring programs. We also provide an overview of future of work publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Cybersecurity

Takeaways from RSA 2022

At the first in-person RSA show since February 2020, we identified several takeaways that reflect how cybersecurity has both changed and stayed the same over the past two years. The complexity of the cybersecurity environment and cybersecurity threats have increased since the beginning of the pandemic. The cybersecurity market grew through the pandemic, and growth probably accelerated. While the outlook is positive, the mood of the conference was that the sector is recession-proof. We think of the market as more recession-resistant and are concerned sentiment will be too bullish should the economy continue to weaken. The shortage of cybersecurity talent continues, leading to weakened security and demand for cybersecurity solutions that enable companies to achieve adequate cybersecurity with fewer internal personnel. The cybersecurity market has become more concentrated among a handful of large players. Software bill of materials (SBOM) is an emerging, interesting area that helps organizations deal with the increasing interdependence of software products and systems. We also provide an overview of cybersecurity publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Internet of Things

Rapid growth ahead for dedicated third-party device management providers

Today, most IoT companies selling proprietary hardware standalone or as part of a complete solution use internally developed software to manage their devices. This is despite the fact device management functionality is fairly standard across vendors, meaning there is little opportunity to add value or differentiate on the basis of capabilities. IoT companies could thus achieve substantial cost savings by buying this software from dedicated device management providers. A handful of companies are now emerging to offer device management software as a service. Given the importance of device management software and the advantages of procuring the software from dedicated third-party providers, we expect these providers to see strong growth in the coming years. We outline what device management software is, the advantages of procuring it from dedicated third parties, and why we think now is the moment for outsourced device management to see substantial adoption and growth. We also profile the leading device management software providers. We include an overview of IoT publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Enterprise productivity

Opportunities for tech providers as automakers increasingly sell direct

While electric vehicle technology grabs auto sector headlines, other substantial changes underway include the shift toward automakers selling directly to consumers and the introduction of alternatives to traditional sales and leasing business models. As this shift continues, we expect to see strong demand for technology that enables automakers to initiate, manage and optimize direct interactions with car buyers and owners. We profile several companies we see as among the leading innovators in the market for such technology, some of which also serve franchise dealers and independent repair shops. Alternative consumption models, such as subscription auto services, appear to be a natural extension of this transformation, representing another compelling opportunity for enabling-technology providers. We also provide an overview of enterprise productivity publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Software as a Service

Valuations plunge despite stronger growth expectations

A group of SaaS companies we consider most relevant for analyzing SaaS company growth expectations provided average 2022 revenue growth guidance of 25.7%, 2.6 points higher than the average for 2021 guidance. Despite this, the average stock price for our broad SaaS universe declined 20.2% in the March quarter, making it one of the hardest-hit groups in the recent market downturn. The average enterprise value multiple of estimated 2022 revenue for the group at the end of the March quarter dropped to 11.2 versus 13.9 last quarter. Given the generally solid guidance provided by our SaaS universe companies, which are also growing much faster than the broad market, we believe investors will migrate back to the sector once they are convinced price bottoms are in place and positive momentum has returned. We provide an overview of SaaS publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Cybersecurity

Demand accelerates in 2021, notably strong growth at larger firms

We present our annual analysis of publicly traded, enterprise-focused cybersecurity firm performance. We highlight that 2021 revenue grew 27%, a notable acceleration from 2020's 19.8% growth and 2019's 20.3% growth, and that actual 2021 revenue exceeded initial guidance by an average 7% and a median 6%, suggesting robust overall demand has only increased. We also highlight the emergence of two giants in the cybersecurity sector, something that hasn't happened previously in the sector's history. With this change, the cybersecurity market structure is for the first time beginning to look more like many other software markets, where a few megacap leaders dominate and many smaller players fill emerging voids. We examine the correlations between top- and bottom-line outperformance and stock price performance. Our analysis of one-, three-, and five-year cybersecurity stock performance through March 28, combined with other elements of our sector analysis, points to prospects for the group to outperform the broader indexes over longer time frames than we've seen historically. We also provide an overview of cybersecurity publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: E-commerce optimization

Brands increasingly embrace g-commerce

Consumer brands and mobile game companies increasingly appreciate the potential to sell real-world goods inside online games. The enormous and diverse nature of the mobile game player user base combined with the large amount of time players spend in games makes online games an outstanding channel for engaging with consumers and generating additional revenue for both brands and game companies. True g-commerce is built around the understanding that players are in the gaming environment to play games, not shop. To that end, g-commerce interactions and transactions happen entirely within games, and g-commerce technologies focus on presenting ads and enabling in-game purchases in ways that are both highly effective and minimally disruptive. We believe g-commerce is gaining momentum and see an increasing number of brands set to launch dedicated initiatives. We highlight key g-commerce-related functions we expect to see broad adoption and profile some of the companies providing these capabilities. We also provide an overview of e-commerce optimization publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Enterprise productivity

Finance automation platforms still winning as enterprises battle to attract, retain finance pros

There is a drought of finance talent across roles and levels, from entry-level to chief financial officer, amidst strong demand. Besides increasing compensation, talent-starved enterprises can compete by making finance roles more intrinsically rewarding with financial automation platforms that enable finance professionals to spend more time on tasks that involve human judgment and creativity. Even ignoring the need to attract finance talent, enterprises see many compelling reasons to invest in financial automation tools. Prominent among them is reducing risk and cost of business disruption due to employee turnover. Platforms that deliver significant value to finance departments include accounts payable and receivable automation and expense management. We highlight several innovative companies in these and related areas. We also provide an overview of enterprise productivity publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Software as a Service

Is the SaaS multiple decline nearing an end?

SaaS stocks declined 8.3% in the December quarter, significantly underperforming the S&P 500's 10.6% gain (and the proxy WCLD is down another 7.5% since Dec. 31). The average enterprise value multiple of estimated 2021 revenue decreased to 18.5 from 20.6 last quarter, which was its peak. At this point, we will start focusing on 2022 and even 2023 multiples. Due to the expected rapid growth of our SaaS universe, the average multiple for 2022 drops to 13.9 from 15.7 at the end of September. Since our last report, we added Certara (CERT), Couchbase (BASE), EngageSmart (ESMT), EverCommerce (EVCM), ForgeRock (FORG), Freshworks (FRSH), Instructure (INST), Paymentus (PAY) and PowerSchool (PWSC) to the universe and removed CornerstoneOnDemand and Medallia due to their acquisition. This brings our SaaS universe to 82 names. We provide an overview of SaaS publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Internet of Things

Wi-Fi sensing: Ubiquitous hardware, improving capabilities suggest mass adoption on the horizon

In our two most recent Internet of Things (IoT) reports, we examined two technologies – cameras and microphones – that can be used in place of traditional sensors to capture data. Here, we continue to explore this theme, moving beyond image and sound to Wi-Fi sensing, or using Wi-Fi networks as sensors. The world is beginning to wake up to the fact that the Wi-Fi devices we use for the simple purpose of accessing the internet and transmitting data actually represent an enormous untapped resource for sensing the environment around us. Wi-Fi’s pervasiveness, both in terms of where it is already deployed and its complete environmental coverage, means it is an inexpensive and flexible resource for “seeing” and measuring the world and gives rise to compelling applications for Wi-Fi sensing in areas like security, automation and wellness. We highlight a few of the companies targeting this emerging market and its transformational potential. We also provide an overview of IoT publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Cybersecurity

Demand for data diodes' extreme security likely to accelerate

Trends and challenges around cybersecurity, critical infrastructure and industrial assets mean there is a growing number of situations where data diodes - network hardware devices that use the laws of physics to ensure a one-way data flow - will be optimal cybersecurity solutions. The decision on whether to use data diodes is typically driven by an assessment of the value of precluding either inbound or outbound data flow versus certain inefficiencies, limitations and costs inherent in using data diodes. While we don't foresee a major inflection point for data diode demand in the near term, we do foresee an eventual tipping point where cost reductions, expanded protocol support and creative solutions to management challenges aggregate to substantially eliminate the tradeoffs for a much broader range of applications and make data diodes a compelling choice. We highlight four data diode vendors that target a variety of constituents in the market. We also provide an overview of cybersecurity publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Future of Work

Freelance marketplaces an essential element of the future talent tech stack

Several forces are converging to make the future of the workforce increasingly fluid. Freelance marketplaces are emblematic of this fluidity, enabling companies and workers to engage far more dynamically than in traditional employment. The benefits of freelance marketplaces for buyers include the ability to quickly scale labor up or down, to quickly and efficiently source highly specialized skills, and to tap a larger talent pool than with traditional employment. Benefits for freelancers include greater flexibility in how, when and where they perform work and often greater earning potential. The emergence of multibillion dollar publicly traded freelance marketplaces highlights the enormous demand. However, there are numerous thriving smaller freelance marketplaces that specialize in one or a subset of related freelance segments that have exciting growth prospects. We summarize how freelance marketplaces work and profile several of these specialized freelance marketplaces. We also provide an overview of future of work publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Enterprise productivity

Tech has emptied offices; it can refill them, too

As the pandemic engulfed the world, workers and businesses found they could function remarkably well by using technology to conduct business almost entirely outside the traditional office. Among the most obvious impacts of this shift is a glut of unused office space. While technology enabled the worker exodus and likely forever changed how and where work is done, it can also help landlords devise and implement new strategies for attracting and retaining tenants in this new world. One area where technology can be key is helping landlords quickly and efficiently reconfigure space to better address companies' new and more fluid space needs. Another area is technology that enhances the value tenants and their employees derive from the space they continue to use. We expect companies that provide these technologies to see strong growth in the coming years as landlords invest heavily to address the substantial changes in the office market. We profile several such companies. We also provide an overview of enterprise productivity publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: E-commerce optimization

To respond to commoditization and sustain growth, point solutions give way to end-to-end strategies

Point solutions have dominated the e-commerce technology market for nearly two decades. With their singular focus on just one component of the e-commerce process, point-solution technology providers can amass deep expertise, concentrate organizational effort, and rapidly evolve to create best-of-breed capabilities. In the past few years, however, the balance has begun to shift toward end-to-end solutions. We see several factors prompting this shift, including commoditization of some point solutions, the drive to sustain or accelerate revenue growth, the need to profitably deploy cash accumulating on balance sheets, diminished concerns about channel conflict, and an increasing appreciation of the value companies can create by owning data streams from multiple e-commerce technology functions. We highlight some of the e-commerce technology areas we think will command the highest valuations and innovative companies leading in these areas. We also provide an overview of e-commerce optimization publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Software as a Service

Mixed quarter for SaaS universe

SaaS stocks gave up most of their September-quarter gains in the month of September but still finished up 3.9% on average, beating the S&P 500, which was essentially flat. The average enterprise value multiple of 2021 estimated revenue increased to 20.6 as of Sept. 30, a new high for 2021 and up from 17.9 at the end of June. However, given the high revenue growth rates in our SaaS universe, the multiple of 2022 estimated revenue was 15.7 (compared to 14.1 at the end of June). In the quarter, we added newly public Confluent (CFLT), Doximity (DOCS), Marqeta (MQ), Monday.com (MNDY), SentinelOne (S), Sprinklr (CXM), Unity Software (U) and WalkMe (WKME) and removed Cloudera and Proofpoint due to their acquisition. This brings our SaaS universe to 74 names. We provide an overview of SaaS publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Cybersecurity

Signs of notable change in federal cybersecurity posture; who stands to benefit?

The U.S. federal government has generated a flurry of orders, pronouncements and guidelines over the past year aimed at helping government entities and the private sector deal with an increasing number of high-profile cyberattacks. The words are remarkably similar to what policy makers have written over the past 25 years. Most would say these policies led to actions that fell well short of their goals. Skeptics say this time will be no different, but we see several signs the current measures will create sustained momentum toward a meaningfully improved cybersecurity posture. We think prospects for this change bode well for companies that can tap into spending by the U.S. federal government as well as those that serve companies that supply and partner with the government, and we highlight some of the potential winners and losers from such a change. We also provide an overview of cybersecurity publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Future of Work

COVID-19 is a lit match in the tinderbox of workforce globalization

Nearly 18 months into the pandemic, no consensus has arisen on the extent to which workers who had previously worked on site will return to working in the office full time, work remotely full time, or do some of each. However, one clear trend we expect to emerge is accelerated workforce globalization: Building a global workforce brings a wide array of challenges, including dealing with myriad cultural practices, labor laws, compliance requirements and tax regulations. Helping employers address these challenges represents a substantial growth opportunity for a new cohort of tech companies that make employing a nationally diverse workforce fast and efficient. We highlight a number of these companies. We also provide an overview of future of work publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Enterprise productivity

Labor, vehicle supply tightness drives more opportunity for tech in auto dealers

The pandemic accelerated dealers' adoption of technology, initially to serve customers during lockdowns and more recently to help provide access to maintenance, parts and other offerings amidst limited availability of vehicles and service personnel. We have observed rapid growth among two main groups of companies that provide this technology via SaaS platforms: customer engagement and diagnostic companies and service technician workflow optimization companies. We briefly profile these two areas and highlight interesting providers in each group. We also provide an overview of enterprise productivity publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Software as a Service

SaaS stocks rebound; how much upside remains?

SaaS stocks recovered in June, finishing the quarter with a 13.2% average gain and beating the S&P 500's 8.2% gain. With the exception of the cybersecurity stocks, our SaaS universe lagged earlier in the quarter as value names generally outperformed growth and momentum stocks in April and May. When longer-term interest rates declined after Federal Reserve comments on June 16, our SaaS universe seemed to get a boost. The quarter-end average enterprise value multiple of 2021 estimated revenue increased to 17.9 from 16.0 last quarter and beat the previous high of 17.6 in December 2020. However, given the rapid revenue growth of our SaaS universe, the multiple of 2022 estimated revenue drops to 14.1. We've added recent initial public offerings (IPOs) Coursera (COUR) and Qualtrics International (XM) to the Future of Work sector and removed Talend (TLND), which agreed to be acquired by Thoma Bravo in March. This brings our SaaS universe to 68 names. We also provide an overview of SaaS publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Cybersecurity

RBVM - key to not getting crushed by the vulnerability boulder

Patching all an enterprise's cybersecurity vulnerabilities is a Sisyphean task that's only made harder by a scarcity of qualified cybersecurity personnel. Risk-based vulnerability management (RBVM) solution providers make it easier for enterprises to protect their business with vulnerability prioritization technology that optimally focuses their remediation efforts on the vulnerabilities that are most important in the context of each business. Several recent events highlight how the RBVM space remains as interesting and important as ever. We examine the considerations related to each of the three elements of the RBVM framework (vulnerabilities, assets and threats), some of the main approaches to RBVM, and some of the companies focused on moving solutions forward. We also provide an overview of cybersecurity publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Internet of Things

Sound monitoring: Overlooked capability offers significant utility

Despite the IoT market's intense focus on video capabilities, we think sound monitoring will garner notable traction driven in part by factors common to all areas of IoT, including declining hardware component and connectivity costs, more flexible and customer-friendly business models and improving technology. We highlight some markets where we think sound monitoring solutions, either standalone or in combination with other sensor technologies, will see strong growth. These include security and surveillance, smart city applications, correctional facilities, smart home and building applications. We also profile players in each of these areas. We also provide an overview of IoT publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Future of Work

Talent acquisition technology: New ammunition in the re-escalating war for talent

After COVID-19 initially created a surge in unemployment last year, the supply of qualified workers relative to demand, which had already been tightening for years prior, resumed its tightening trend. One indicator of the imbalance hit its highest level in the past 15 years in April 2021. In some ways, COVID-19 exacerbated the tightening trend despite the economic dislocations it caused. As power in the skilled labor market shifts further to the supply side and employers increasingly compete for the best talent, technologies that help employers effectively find and attract the talent they need are more critical than ever. We discuss two companies that provide such technology: newly publicly traded ZipRecruiter (ZIP) and privately held Visage, a new First Analysis portfolio company. With no sign of a cease-fire in the war for talent anytime soon, we anticipate robust demand for such technologies. We also provide an overview of future of work publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Enterprise productivity

Ensuring a better insurance market with InsurTech

The insurance industry historically has been characterized by manual processes, large agent-based sales forces, and slow, arbitrary and contentious claims processing. Increasingly, industry participants are using technology to automate the business. Myriad technology solutions add value for carriers, brokers, and insureds by improving underwriting efficiency, product quality, and claims processing speed and accuracy and by reducing insurance portfolio risk. We group these solutions into four categories based on their primary focuses: sales and underwriting, policy administration, claims processing, and risk management, and we highlight some of the interesting technology providers in each group. We also provide an overview of enterprise productivity publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Software as a Service

SaaS universe guidance looks conservative again for 2021

The 22.3% average 2021 revenue growth guidance for our SaaS universe (excluding vertical SaaS and other) is 9.6 points lower than average actual 2020 revenue growth. Typically, this initial guidance proves conservative. Even in the pandemic year of 2020, actual growth was 4.6 points better than initial guidance that suggested 2020 revenue growth would be 10.9 points less than in 2019. As we have noted before, we believe the pandemic reduced the average growth rate for our SaaS companies by 5-6 points (albeit with some notable variance among the constituents). We have added recent IPO C3.ai (AI) to our SaaS universe and removed Pluralsight (PS) and Slack (WORK), both as a result of acquisition. In March, Talend (TLND) agreed to be acquired by Thoma Bravo for $66.00 per share. SaaS stocks gave back gains in the second half of the March quarter after a strong start to the year. With market momentum shifted to value names, our SaaS stocks dropped an average 8.4% for the March quarter compared to a 5.8% gain for the S&P 500. We discuss these changes and also provide an overview of SaaS publicly traded stock performance and valuation.

|

Quarterly insights: E-commerce optimization

Brands using smartphones to step up direct consumer engagement

Brands deeply desire to be close to consumers but have avoided selling direct until recently for fear of upsetting traditional distribution partners. The tide has begun to turn as brands have stepped up online consumer engagement and direct sales efforts while increasing investments in technology. The ubiquity of smartphones and their increasing native support for legacy technologies such as QR codes and NFC tags suggests we are at an inflection point toward much greater direct consumer engagement by brands through physical objects, such as their products and signage, and significant investment in technology to enable these efforts. COVID-19 has also accelerated consumers’ embrace of online interactions and shopping. We believe most brands will subscribe to third-party technologies to ramp up their digital direct engagement efforts. We highlight several innovative technology providers supporting direct interactions that are likely to profit from this dynamic. We also provide an overview of e-commerce optimization publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Cybersecurity

Not a micro segment: Microsegmentation's ability to protect the cloud is big opportunity

As bad actors have learned to take advantage of the freedom inside a protected environment and internal threats have become better understood, cybersecurity spend has rapidly expanded from protecting internal assets from outsiders to better controlling lateral data flows within protected environments. In a world where lateral data flows for a business process can now span on-premise infrastructure, a company’s own data center, third-party data centers such as AWS, Azure, and Google Cloud, and hosted cloud applications from third parties, microsegmentation is a key solution in the arsenal to protect business assets. While microsegmentation can be highly effective and has great promise, its relatively early stage of evolution combined with its complexity mean there is a long runway for the market to grow as innovative cybersecurity companies invest to introduce better solutions. We highlight just a few of the companies providing some of today’s leading solutions. We also provide an overview of cybersecurity publicly traded stock performance and valuation, sector M&A activity, and private placements during the quarter.

|

Quarterly insights: Future of Work

Employee benefits: Key to taming the long tail on the COVID beast